The democratization of financial information and removal of trade barriers has had a beneficial effect on improving market efficiency in developed economies. In this context, stock prices are assumed to reflect expectations of a company’s future performance. But what happens when investors stop making rational decisions and emotion begins to drive market behavior?

When Emotion Becomes a Market Force

One of the interesting financial phenomena to emerge in the 2020s is the rise of the “meme stock”: these securities experience rapid and significant price movements driven by retail investors’ actions rather than changes in fundamentals. Meme stock trading activity tends to be concentrated among individual retail investors, often organized through social media platforms, and are characterized by a high level of emotional decision making. Fear of missing out on gains, herding behaviors, and speculative activity decouple stock prices from their intrinsic value.

At the same time, consumers base their purchasing decisions on multiple factors, one of them being their perception of the brand itself. The existence of brand premia, or the fact that certain brand name products can command a higher price than an otherwise identical generic substitute through the sheer power of marketing, suggests that purchasing decisions are influenced to an extent by emotional considerations. The Harris Poll’s QuestBrand platform calculates a Brand Equity Index incorporating four such factors: momentum, consideration for future purchase, quality of its goods and services, and familiarity.

Testing Whether Emotion Can Predict Markets

In this context, we investigated whether incorporating brand emotion metrics into a traditional financial valuation framework could improve forecasts. We hypothesized that the impact would be greater among meme stocks. For our analysis, we leveraged three long short term memory (LSTM) models: one that incorporates financial metrics only, one that utilized brand metrics only, and one that combined the financial and brand metrics.

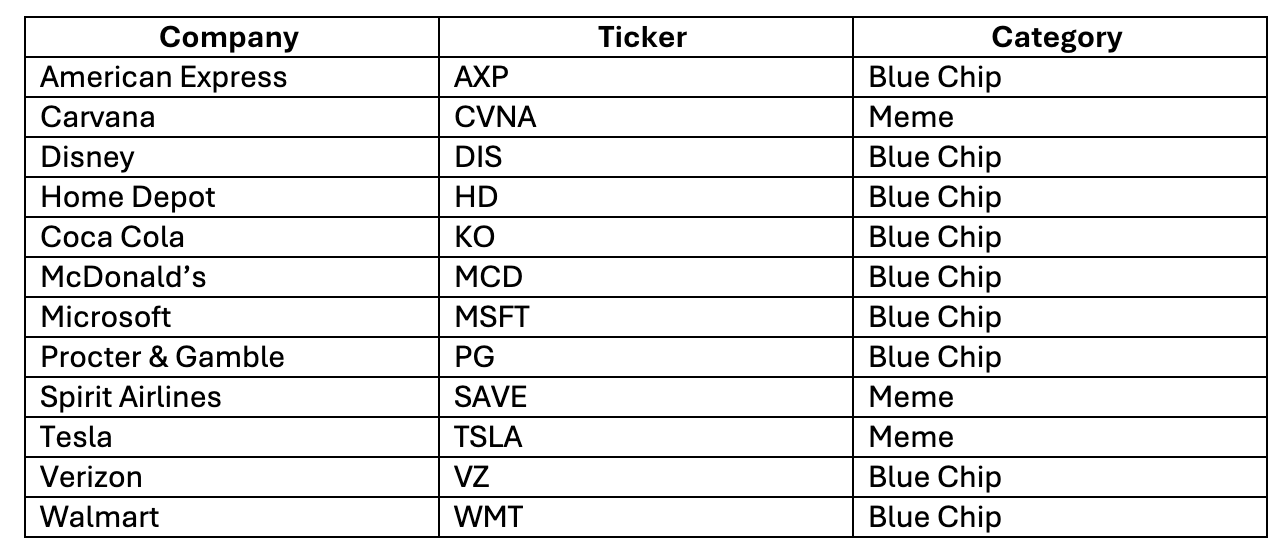

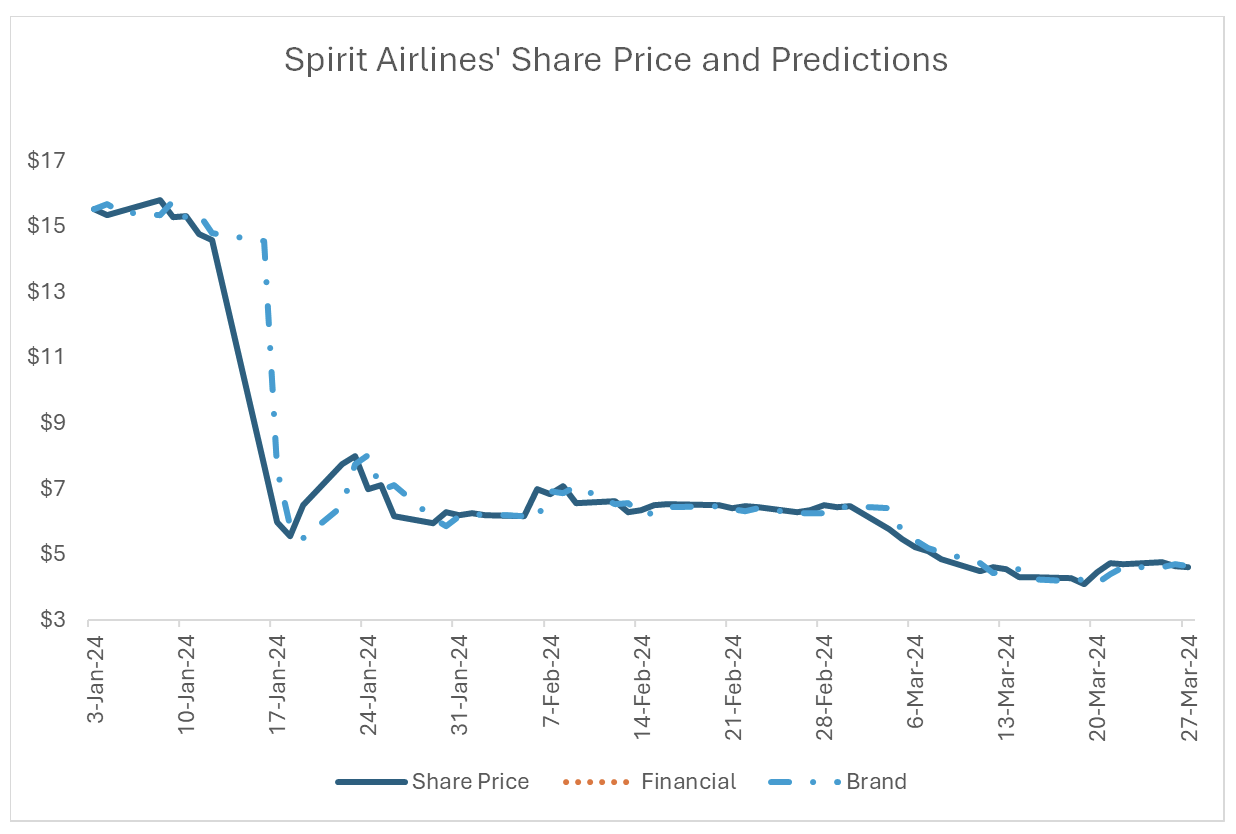

Our sample was made up of twelve publicly traded equities for which QuestBrand data was available: 9 components of the Dow Jones industrial average in differing industries, and three “meme” stocks that were part of the Solactive Roundhill Meme Stock Index. We trained each model on daily data spanning 2021 to 2023 and attempted to predict stock prices for Q1 2024 on a one-day-ahead basis.

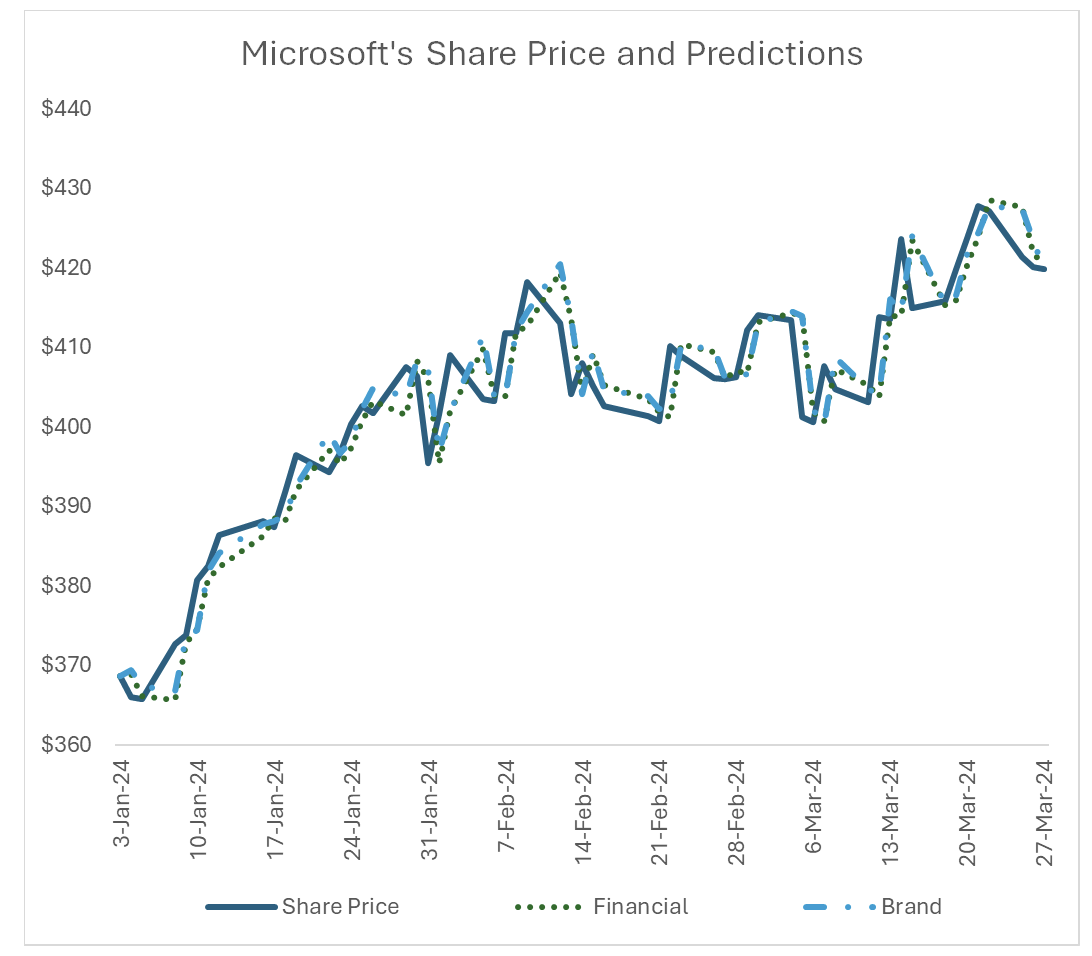

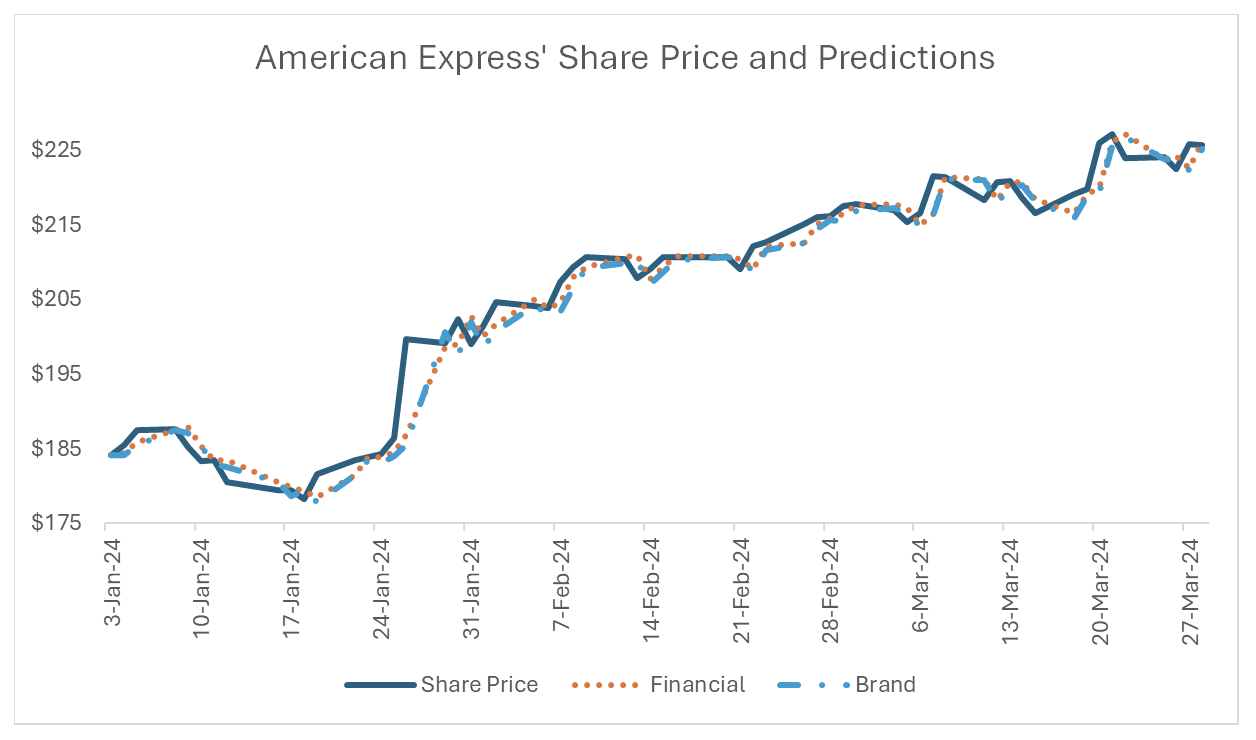

The results of the experiment were mixed, with neither of the three models emerging as a clear favorite. Across our 12 firms, the brand model produced the smallest mean absolute error for 6 brands, the financial model was the best for five brands, and the combined model came out on top for one brand. Looking at correlations between predictions and realized values, the financial model was the best for four brands, the brand model excelled for three, and the combined model returned the highest correlation for five brands.

Interestingly, all three meme stocks achieved their smallest MAE and highest correlations in the financial metrics model, contradicting our hypothesis. This could however be an artifact of the small sample. That said, there is no statistical difference between the financial model and the combined model in terms of fit and accuracy, suggesting that incorporating brand metrics does not enhance predictability.

The Takeaway: Emotion Matters — But With Limits

We subsequently ran a perturbation analysis to identify the most important factors for the prediction. In the vast majority of cases, the most impactful attributes were brand related, not financial metrics. Momentum, defined as a respondent’s outlook of the brand’s future performance, emerged as the second most important factor overall, which concords with the theory that stock prices reflect expectations of the future.